Unexpected car repairs have a way of arriving at the worst possible time. Your transmission gives out the week before rent is due, or your brakes fail right after you’ve cleaned out your savings. Understanding how auto repair financing works can be the difference between getting your car fixed today and watching it sit in the driveway for weeks. This guide breaks down every major financing option available to you, explains what interest rates and fees actually mean for your wallet, and gives you a clear path from “I need repairs” to “my car is fixed and I have a payment plan I can manage.”

Table of Contents

- Key takeaways

- How auto repair financing works: the basics

- Understanding interest rates, APR, and fees

- How to apply for auto repair financing

- Comparing your financing options

- Practical tips for managing repair financing

- My honest take on auto repair financing

- Repair financing made easy at Kwik Kar Oil Change & Auto Care

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Multiple financing options exist | Personal loans, credit cards, shop payment plans, and dealer programs each work differently and suit different budgets. |

| APR range is wide | Interest rates vary from 0% promotional offers to as high as 35.99% depending on creditworthiness. |

| Start with a written estimate | A detailed repair estimate helps you borrow the right amount and avoid funding gaps mid-repair. |

| Promotional 0% APR has strings | Deferred interest kicks in if you carry a balance past the promotional window, erasing the benefit entirely. |

| Match terms to your payoff ability | Choose a loan term length you can realistically meet to avoid unnecessary interest and fees. |

How auto repair financing works: the basics

Auto repair financing generally means borrowing money upfront to pay for vehicle repairs, then repaying that amount over time through fixed or flexible installments that include interest. Think of it as separating a large repair bill into smaller, more manageable pieces spread across weeks, months, or even years.

There are four main categories of auto repair financing options you will encounter:

- Personal loans: A lender gives you a lump sum of cash after approval. You repay it in fixed monthly installments that include both principal and interest. These are typically unsecured, meaning your car is not used as collateral. Terms range from a few months to several years.

- Credit cards: If you have a card with available credit, you can charge the repair directly. Cards with a 0% introductory APR offer a window of interest-free repayment. Miss that window, and standard card rates apply.

- Repair shop payment plans: Many shops partner with financing companies to offer point-of-sale plans you apply for right at the counter. Applications process within minutes on a phone or tablet, often with high approval rates and softer credit checks.

- Dealer or manufacturer financing: If your car is under warranty or serviced at a dealership, some manufacturers offer their own financing programs tied to specific service centers. These tend to have fast approvals but can carry higher overall repair costs.

Each path has different approval speeds, interest structures, and credit requirements. The best fit depends on your credit profile, how urgently you need the repair, and how much flexibility you need in repayment.

Understanding interest rates, APR, and fees

APR stands for Annual Percentage Rate. It reflects the yearly cost of borrowing, including interest and certain fees, expressed as a single percentage. The interest rate alone tells you how much you are charged on the principal. APR gives you the fuller picture.

Here is what you need to know about the cost structure of auto repair financing options:

- 0% promotional APR: Some shop financing programs and credit cards advertise 0% APR for a set period. This is genuinely interest-free, but only if you pay off the entire balance before the promo window closes. Many of these offers carry deferred interest conditions, meaning if any balance remains at the deadline, back-interest on the full original amount gets added to your bill.

- Standard APR range: Rates on auto repair loans and financing plans can stretch from below 10% for strong credit borrowers to as high as 35.99% for those with limited or damaged credit histories.

- Origination fees: Some personal loan lenders charge an upfront origination fee, typically 1% to 8% of the loan amount, deducted before you receive your funds. This effectively raises your borrowing cost even if the stated interest rate looks reasonable.

- Late payment fees: Missing a payment can trigger penalty fees and potentially trigger a higher penalty APR on certain credit products.

Your credit score plays a direct role here. A score above 700 typically unlocks the lowest APR tiers. Scores below 600 narrow your options and push rates higher.

Pro Tip: Before you sign any financing agreement, verify the final APR, all fee disclosures, and repayment terms in writing. A verbal promise of “low interest” means nothing if the contract says something different.

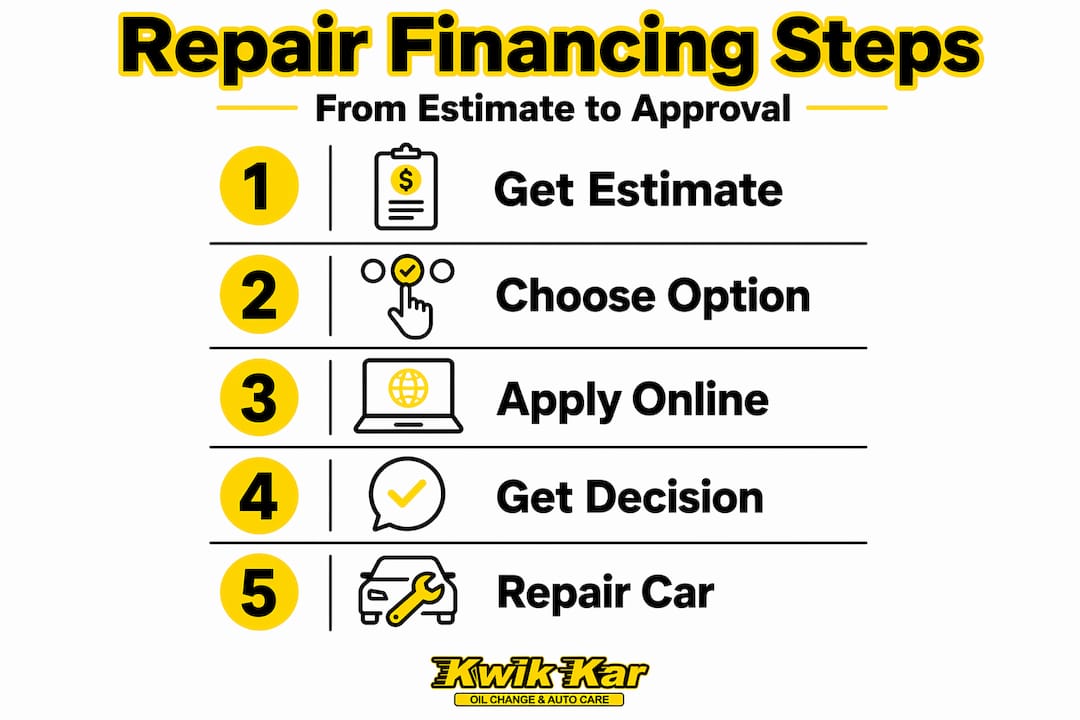

How to apply for auto repair financing

The process for how to finance car repairs is more straightforward than most people expect. Here is what a typical application looks like from start to finish:

Get a written repair estimate. Before you apply for anything, ask the shop for a detailed written estimate. Starting with a written estimate is the most reliable way to borrow the right amount and avoid scrambling for additional funds if the repair runs over your initial loan.

Compare your financing options. Do not accept the first offer presented to you at the counter. Check whether a personal loan from your bank or credit union offers a better rate than the shop’s in-house plan. Even spending 20 minutes comparing can save you hundreds of dollars over the life of the loan.

Prequalify where possible. Many lenders let you check your likely rate using a soft credit inquiry, which does not affect your credit score. This gives you a realistic picture of your options before you commit to a hard credit pull.

Submit your formal application. Once you have selected a lender or financing option, complete the full application. In-shop point-of-sale financing tends to approve applicants quickly, often within minutes. Personal loan funds typically arrive within one to three business days after approval.

Review the loan agreement carefully before signing. Confirm the APR, total repayment amount, monthly payment, term length, and any fees. Then authorize the repair to begin.

Start repayment as scheduled. Set up automatic payments if possible to protect your credit and avoid late fees. Track your balance against any promotional payoff deadlines.

Comparing your financing options

Each option has genuine strengths and real drawbacks. Here is a direct comparison to help you think through the decision:

| Option | Best for | Watch out for |

|---|---|---|

| Personal loan | Larger repairs, fixed budget planning | Approval time of 1-3 days, origination fees |

| Credit card (0% intro APR) | Quick approval, rewards earning | Deferred interest if balance remains at promo end |

| Shop payment plan | Immediate approval, lower credit bar | Variable terms, potentially higher overall cost |

| Dealer/manufacturer financing | Warranty repairs, convenience | Higher repair labor rates at dealerships |

| Car title or payday loan | Last resort only | APRs up to 400%, repossession risk |

A few additional points worth keeping in mind:

- Personal loans typically carry lower interest than credit cards when used outside a 0% promo window, making them the better long-term choice for repairs over $1,000.

- Repair shop plans often approve applicants who have been declined elsewhere, which makes them a practical option for people rebuilding their credit.

- Dealer financing is convenient when your vehicle is already at the dealership, but the combination of higher shop labor rates and financing costs can make the total bill significantly larger than at an independent shop.

- Car title loans deserve their own warning. With average APRs around 300% and a real risk of losing your vehicle, they should be treated as a last resort, not a convenient shortcut.

Practical tips for managing repair financing

Knowing your options is only half the battle. Using them wisely is where most car owners either save money or lose it.

Pro Tip: Compare total interest and fees across your financing routes before committing, not just the monthly payment. A lower monthly payment stretched over a longer term often costs more in total than a slightly higher payment over a shorter term.

Here are the most important practical guidelines to follow:

- Match the loan term to your realistic payoff timeline. If you can clear the balance in three months, a short-term shop plan may work perfectly. If you need 18 to 24 months, a personal loan with a defined term and fixed rate gives you more stability.

- Build a payoff plan before you accept a 0% APR offer. Divide the total balance by the number of months in the promo period. If that monthly number exceeds your budget, the 0% offer will likely backfire.

- Ask every shop about in-house financing. Many repair centers have financing arrangements you will never hear about unless you ask. Some shops offer better terms to repeat customers or will waive certain fees.

- Check your existing accounts first. If you have a personal line of credit, a low-APR credit card, or a home equity line, those may offer better rates than any new financing you apply for.

- Do not overlook non-urgent repairs. If a repair is not safety-critical, delaying it by 30 to 60 days while you save cash can eliminate the financing cost entirely. Understanding car maintenance basics can help you identify which repairs are urgent and which can wait.

My honest take on auto repair financing

I have seen a lot of car owners get burned not by financing itself, but by the pressure of the moment. When you are standing at a service counter and your car is already in pieces, the offer of instant approval feels like relief. That rush to say yes is exactly when you need to slow down.

In my experience, the monthly payment number is the single most misleading figure in any financing conversation. Lenders and shops know that people approve purchases based on what feels manageable each month. What they do not always volunteer is the total cost of the loan once interest and fees are added across the full term. I have watched a $900 repair become a $1,300 financial obligation because someone accepted a long-term plan without running the numbers.

Promotional 0% APR offers are genuinely useful, but only for people who plan their payoff from day one. Without a concrete plan, that offer is really just a delayed interest charge waiting to happen. Knowing how to build a zero-balance payoff plan before the promo ends is what separates smart borrowers from regretful ones.

The relationship you build with a trusted repair shop also matters more than most people realize. Shops that know you, know your vehicle, and have earned your repeat business are often willing to work with you on payment terms, flag unnecessary repairs before they become emergencies, and connect you with the most favorable financing options they have access to. That kind of trust does not come from a quick Google search. It comes from consistency. Sometimes the smartest financial decision is simply paying cash for a smaller, non-urgent repair now, so that you preserve your financing options for when a genuinely large repair demands it.

— Kwik Kar

Repair financing made easy at Kwik Kar Oil Change & Auto Care

When a repair bill catches you off guard, you deserve both quality service and a payment path that fits your situation. Kwik Kar Oil Change & Auto Care provides full auto repair services backed by ASE Certified Master Technicians and recognition from RepairPal and NAPA AutoCare. Every repair starts with transparent diagnostics and a written estimate before any work begins, so you always know exactly what you are paying for before you commit.

Kwik Kar’s certified repair team works with you to explain your financing options directly at the shop, including available payment plans that fit your timeline. Whether you need a same-day fix or want time to compare your options before scheduling, Kwik Kar is ready to help. Schedule your appointment today and get the repair process started with a shop that puts transparency and affordability first.

FAQ

What is auto repair financing?

Auto repair financing is borrowing money upfront to cover vehicle repair costs, then repaying that amount over time through installments that include interest. Options include personal loans, credit cards, and in-shop payment plans.

Can you finance car repairs with bad credit?

Yes. Point-of-sale shop financing plans often approve applicants with lower credit scores and use softer credit checks than traditional lenders. Approval rates at the shop level are generally higher than at banks or credit unions.

How does a 0% APR repair financing offer work?

A 0% APR offer means you pay no interest during the promotional period, typically three to eighteen months. If any balance remains when that period ends, back-interest on the full original amount is usually added to your account.

What APR should I expect on auto repair loans?

APR on auto repair financing options ranges from 0% on promotional offers to as high as 35.99% depending on your credit score and the lender. Borrowers with strong credit qualify for significantly lower rates.

How long does it take to get approved for repair financing?

In-shop point-of-sale financing approves most applicants within minutes. Personal loan funds from an outside lender typically arrive within one to three business days after a formal application is approved.